- Not insured by the FDIC or any other government agency

- Not bank guaranteed

- Not a deposit or obligation

- May lose value

Data from a Gallup Poll currently shows that less than half of U.S. adults have a will, with the percentage increasing based on factors such as age, income, and education. Despite the numbers, know that some form of estate planning is essential for everyone. The planning process allows you to determine what happens to your assets and can provide you and your family’s protection in cases of medical emergency and end-of-life care. However, you may feel overwhelmed with where to begin.

Our 5-step guide on estate planning will give you a thorough yet easy-to-follow overview of the process. You’ll be able to take what you learn here and translate it into building an estate plan that gives you peace of mind. Let’s begin.

No matter your age or net worth, the first step in any financial, retirement, or estate planning process is to take a moment to organize your affairs. This means identifying, collecting, and reviewing the current state of your finances. Compiling your financial information upfront helps you identify questions for your estate planning team and allows them to advise you with the most recent and accurate information possible.

Start by listing out all your assets and liabilities along with their values to get an approximation of your net worth. Your assets and liabilities will likely include one or more of the following:

Also, consider if any of your assets or liabilities are subject to change in the short term or while you are in the process of creating your estate plan. For example, buying or selling a piece of real estate. Changes in your assets could impact the estate planning options at your disposal.

Estate planning is a collaborative effort requiring input and personalized attention from several key parties you trust. While everyone’s estate planning team may look different, this group of professionals may include your:

Each of these professionals plays a significant role in creating a holistic estate plan that is legally sufficient, consistent, and that addresses your goals. The members of your team must communicate and work together to provide you with estate planning guidance as it relates to their areas of expertise.

With your estate planning team assembled, your next step is to consider what you want your plan to accomplish. Estate planning often provides a unique blend of financial and personal objectives that require a delicate balance of emotion and logic in decision-making. Carefully considering and prioritizing your various goals will help you create a plan that best reflects your intent with your family, finances, and legacy.

General goals that individuals and families may find relevant in driving their estate planning are:

Understanding your goals before creating your estate plan will help you make informed decisions about the structure of your plan (i.e., who receives what assets and when).

After considering your goals, it will be time to execute your estate plan. This step will look slightly different for everyone depending on their assets, family, and plan but will generally involve some combination of the following documents, in addition to others:

Most estate planning tools (e.g., a will, trust, power of attorney, etc.) require the help of someone in a fiduciary position to fulfill the terms of your estate plan. Depending on the document, this could be a personal representative, executor, trustee, etc. The people chosen to fill these roles are often a spouse, adult child, close friend, relative, or professional group. Consider appointing successors for the various functions in your estate plan if one or more of your fiduciaries is unable to serve when the time comes.

The help of your estate planning team will be critical when it comes to completing and signing the necessary documents that finalize your plan. Your documents must be fully executed (i.e., signed and compliant with other legal requirements such as having proper witnesses). You might also need to retitle certain assets into your trust if you created one.

Finally, some of your assets may have payable on death (POD) or transfer on death (TOD) forms that you will need to review and possibly change to ensure they fit with your newly created plan. This could be a life insurance policy, bank account, or investment/retirement fund. Many are surprised to learn that assets with these forms will operate outside of their estate planning documents.

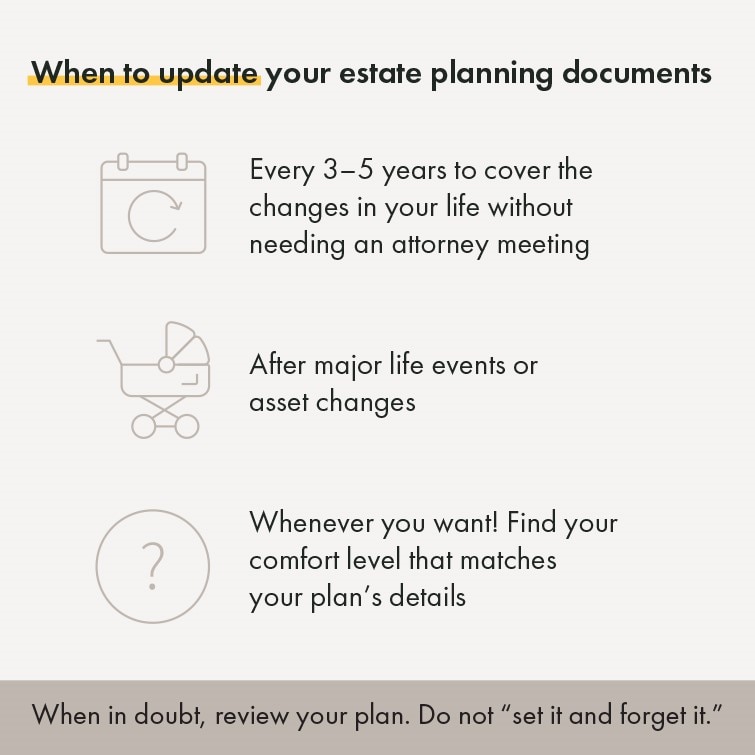

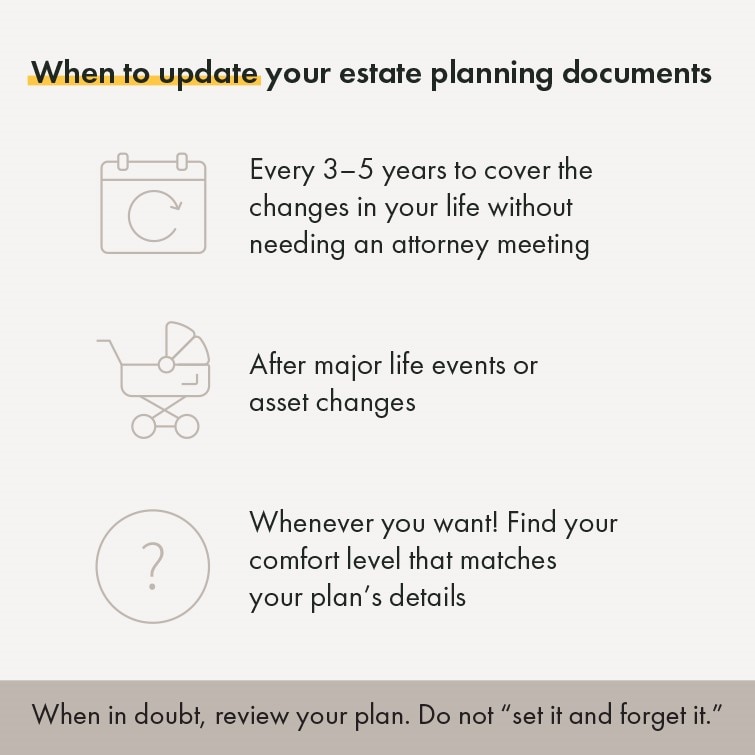

Another common misconception about estate planning is that it is a process you do once and then never think about again. Unfortunately, estate plans do not operate in a vacuum. Changes in your assets, life circumstances, or the law can significantly impact how your estate plan operates and the effect it has. Revisit your estate plan occasionally and see if any life events would necessitate an update. For example, buying or selling a significant asset, marriage, divorce, death, etc.

The team at Yellow Cardinal Advisory Group is eager to help clients navigate the estate planning process together. Fiduciary officers are trained to understand and interpret estate planning guidelines to find the approach that best suits each client.

Contact Yellow Cardinal Advisory Group to explore how our estate settlement and trust administration services can support your estate planning goals.

Estate Planning Image: Adapted from “When to Update Your Estate Planning Documents,” by Financial Residency; https://financialresidency.com/when-and-why-you-update-estate-documents/

The information on this page is accurate as of March 2022 and is subject to change. First Financial Bank is not affiliated with any third-parties or third-party websites mentioned above. Any reference to any person, organization, activity, product, and/or service does not constitute or imply an endorsement. By clicking on a third-party link, you acknowledge you are leaving bankatfirst.com. First Financial Bank is not responsible for the content or security of any linked web page.

You are about to go to a different website or app. The privacy and security policies of this site may be different than ours. We do not control and are not responsible for the content, products or services.

Online banking services for individuals and small/medium-sized businesses.

If you haven't enrolled yet, please enroll in online banking.

Yellow Cardinal resources

* Are not insured by the FDIC. Not a deposit. May lose value.

For businesses already using f1RSTNAVIGATOR online banking.

For clients joining from BankFinancial, Westfield Bank or opening a new business account after April 15, 2026.