short-term goals lead to big savings: the 12-week savings challenge

A savings challenge is a great way to work on your budgeting skills while saving money along the way. This 12-week savings challenge is easy, fun, and effective.

Table of Contents

- Set a goal

- Make a budget and stick to it

- Use apps to help

- Meal plan with store brands

- Subscriptions the smart way

- A night in doesn't mean skipping the fun

- Shop around for necessary bills

- Use the 24-hour rule

- Don't overlook community events

- Stay out of *that* store

- Pay off your credit card in full

- Try a no-spend month

Whether you're dreaming of a vacation, looking to ease your money stress, or just want to build a little rainy day fund, we have a fun and simple way to jumpstart your goals with a 12-week savings challenge.

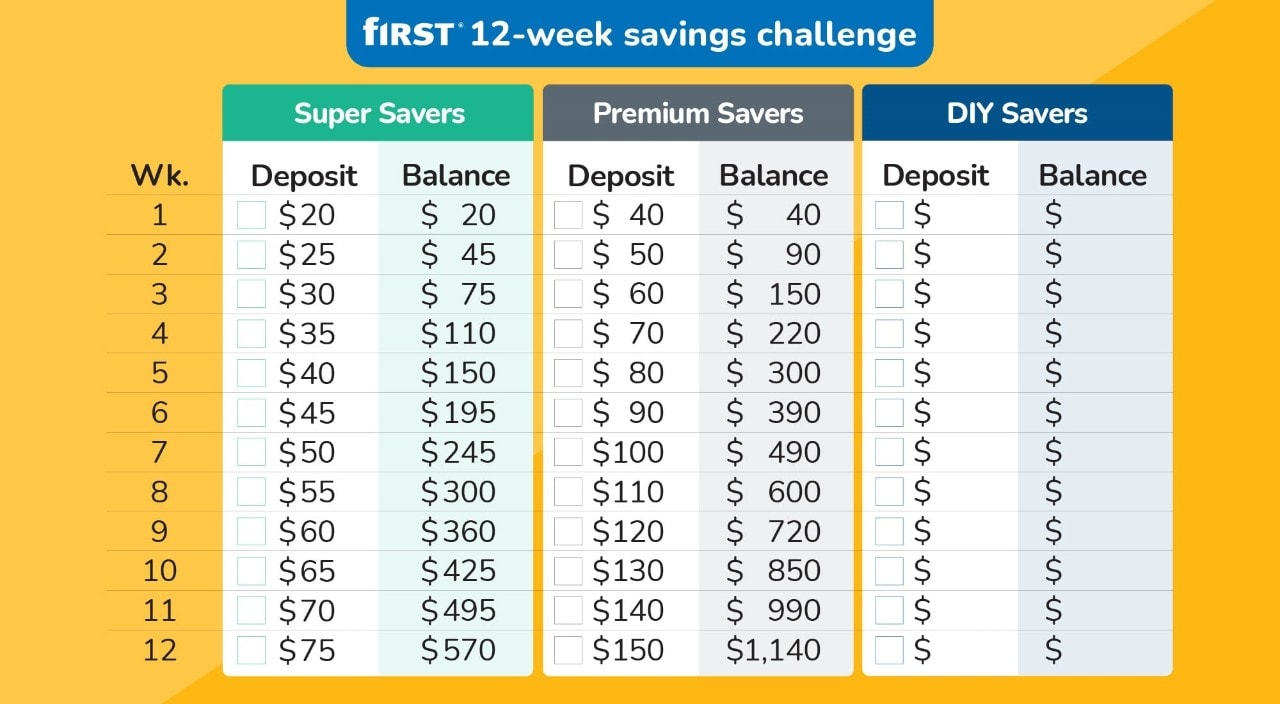

Start in September and you’ll be done just in time for the holiday season. There are three challenge levels to choose from (including one you can fully customize), so you can pick the option that works best for your budget and goals.

Let’s take a look at the three 12-week savings challenge options and get started today.

Did you know it takes 59 to 70 days to create a habit?

It’s no coincidence this challenge runs for 84 days. We want to help you create a savings habit. Smart saving skills begin with making saving money a habit to help take control of your finances. By the end of this challenge, you’ll have honed the skills you need to make saving money second nature, without needing to bruise your fingers pinching pennies.

Even if you’ve never made a budget before or tried time and time again to stick to your budget but never saw results, we can help change the way you think about money.

Ready to take the challenge? Don’t miss these 12 tips:

1. Set a goal

Ask yourself, what am I saving for? Setting a clear goal is the first step to making sure you get the most out of this year’s savings challenge. You’ll want to make sure the goal is exciting or powerful enough for you to stay motivated. You may want to make holiday shopping less stressful this year, build your emergency fund, or even jumpstart saving for a downpayment on a home. Finding your reason “why” is totally up to you!

When you set your goal, it is helpful to follow the SMART framework to increase your odds of success:

- Specific – Make your goal targeted and detailed

- Measurable – How will you measure success? Can you track your progress?

- Achievable – Make sure you can accomplish your goal in a certain time frame (maybe over 12 weeks).

- Realistic – Your goal should be something you can truly accomplish and that you can control.

- Time-based – Having an end date in mind to accomplish your goal increases your motivation and makes success easier to quantify.

Here’s an example of a vague goal compared to a smart goal:

- Vague goal – I want to save more money this year.

- SMART goal – I’m going to save more money by tracking my expenses, creating a 50-30-20 budget, and saving an extra 10% of my paycheck each month.

2. Make a budget and stick to it

There’s no way to avoid it; to achieve your savings goals, you need a budget. There are a few methods out there, but we are big fans of the 50/30/20 method. Here’s how it works:

Needs = 50% of your income should go to the necessities you can’t live without. Your housing, food, transportation, insurance, and utilities are all examples of necessities.

Wants = 30% of your income goes towards things you want. This 30% is the type of lifestyle you live. Make sure you know the difference between wants and needs when managing this part of your budget. Things like monthly subscriptions and eating out are wants, not needs.

Savings = the final 20% of your income should go towards saving money for your future. These savings should also include building an emergency fund if you don’t have one.

3. Use apps to help

There are a variety of apps out there that help you manage your budget and track your spending. Let’s be realistic, nobody has time to track every penny they spend on a piece of paper or in a spreadsheet. Using an app allows you to automatically categorize expenses and shows you a visual representation of where your money is going.

A great example of an app you can use to manage your money is our Insights tool. The best part? Insights comes free with all of our checking and savings accounts and is found within our banking app. You can create a budget or upload a version of your current budget and sort your spending by category and even set up goals to track your progress. Tracking goals is perfect for a savings challenge like this. Don’t forget to link any other accounts you may have at another bank or credit union including your loans and credit cards to Insights so you can get a complete view of all your finances in one place.

4. Meal plan with store brands

Prices at the grocery store are high right now, but there are still a few ways you can save some money without skimping on quality food. The best way to avoid buying unnecessary or extra food is to come up with a meal plan each week. You are more likely to overspend when you don’t have a list. When you are coming up with a list, don’t forget to shop around for sales and coupons. When you have a well thought out list, shopping is a breeze because you already know exactly what you need to get.

Don’t sleep on store brands either. Most stores have their own versions of popular products at much lower prices. These store brands are a great way to get high quality food at a price that’s easier on your wallet.

Buying in bulk is a strong way to save money on non-perishable items. You’ll buy more than you need up-front, but at a lower price per item. Things like toothpaste, toilet paper, and canned food are good things to buy this way.

5. Subscriptions the smart way

Here are some numbers on subscription services like gyms, streaming services, and apps:

- 4.5 – the average number of subscription services an American has.2

- $924 – the average amount of money people spend on subscriptions services per year.2

- 54 – the percentage of people that underestimate their subscription costs by more than $100.3

Subscriptions make it easy to access media and tools we want, but they also make it easier to waste your money when you forget to cancel or subscribe to too many services. It’s easy to forget about subscriptions because you usually provide your debit or credit card once and you are automatically charged each month. We recommend ditching the subscriptions you don’t use at least once a week.

6. A night in doesn't mean skipping the fun

It’s important to leave room in your budget to treat yourself, or you will have a tough time sticking with it. Replacing just one happy hour will save you a chunk of change, but that doesn't mean you can’t still have fun. Inviting your friends over for a potluck dinner is just one example of how you can still have social time without overspending on expensive food and drinks.

7. Shop around for necessary bills

There’s more value than you think in giving your phone or cable provider a call. You may dread waiting to talk to a service representative, but this is a great way to ensure you aren’t paying for any extras you don’t need.

It also pays to shop around for new insurance, phone, and cable providers when your current contract is up. Many companies offer incentives for new customers to leave their old provider. A little bit of time investment on your end can lead to big savings.

8. Use the 24-hour rule

Retail therapy is a popular way de-stress after a long week at work, but the price of these therapy sessions can really add up. Instead of getting on your favorite shopping website, check out a new park, hiking trail, or just unwind in one of your favorite free places.

Try the 24-hour rule if your retail spending is hard to manage. Put whatever item you are thinking about buying in your online cart, but wait 24 hours to hit buy now. You’ll find that in 24 hours, you may not still feel the urge to spend that money.

9. Don't overlook community events

Even though you’ve made some lifestyle changes when it comes to how you spend your money, you don’t have to avoid fun and social events. A great way to find free events is to check out the websites for your community and the communities around you. It doesn’t hurt to keep an eye on the social media accounts for local parks either. These organizations typically host free events with interesting activities.

Another option is finding some local volunteer opportunities. These are a unique way to meet new people and socialize, all while saving money and giving back.

10. Stay out of *that* store

Look…we all have one store. The one we always seem to spend way more than we mean to spend on impulse purchases way too frequently. Making a conscious effort to stay out of the store or stores where you find yourself spending way more than you want to for a set period of time is a great way to save money.

Depending on how frequently you visit your guilty pleasure store, you may want to set a one week time limit or even a month-long goal. Even recognizing which stores lead you to impulse buy is a huge step in the right direction.

11. Pay off your credit card in full

Are you paying off your credit card in full each month? The average monthly credit card interest fee is $110.50, which is a huge chunk of money that you could be saving or using for your other financial goals.4

Even though credit cards are a great tool to earn points or rewards for spending you were already planning on doing, it’s important to pay your balance at the end of each month, before interest fees kick in. Avoiding the temptation to overspend on your credit cards will make it easier to pay your balance each month, and can even lead to a healthier credit score.

12. Try a no spend month

The final tip for the 12-week savings challenge is really an extension of the challenge itself. If you’ve made it this far, you’ve made tons of changes in the way you manage your money and might find yourself looking for a new, bigger challenge. A no spend month isn’t exactly what it sounds like. The concept is simple: Only spend money on the things you absolutely need for one full month.

This means you are free to spend on the necessities and your bills, but try to minimize or even eliminate any extra spending outside of that. It’s a big challenge, but one that you may find leads to a huge increase in your savings account at the end of the month. Some people choose to completely eliminate spending outside of the necessities for a month, but some people adapt the challenge to allow for spending on certain days. You can customize the concept to whatever best fits your needs!

Budgeting and savings challenges aren’t about restricting yourself. They are about developing lifelong skills to give you more financial freedom, not less. Whether you try the Super Savers, Premium Savers, or DIY Savers challenge, one thing is certain: you’ll have more money saved at the end than when you started.

If you think you’ll need help meeting your weekly goals, ask someone else to take the challenge with you! The more people in your life working on developing the same skills, the easier it’ll be to hold each other accountable.