- Not insured by the FDIC or any other government agency

- Not bank guaranteed

- Not a deposit or obligation

- May lose value

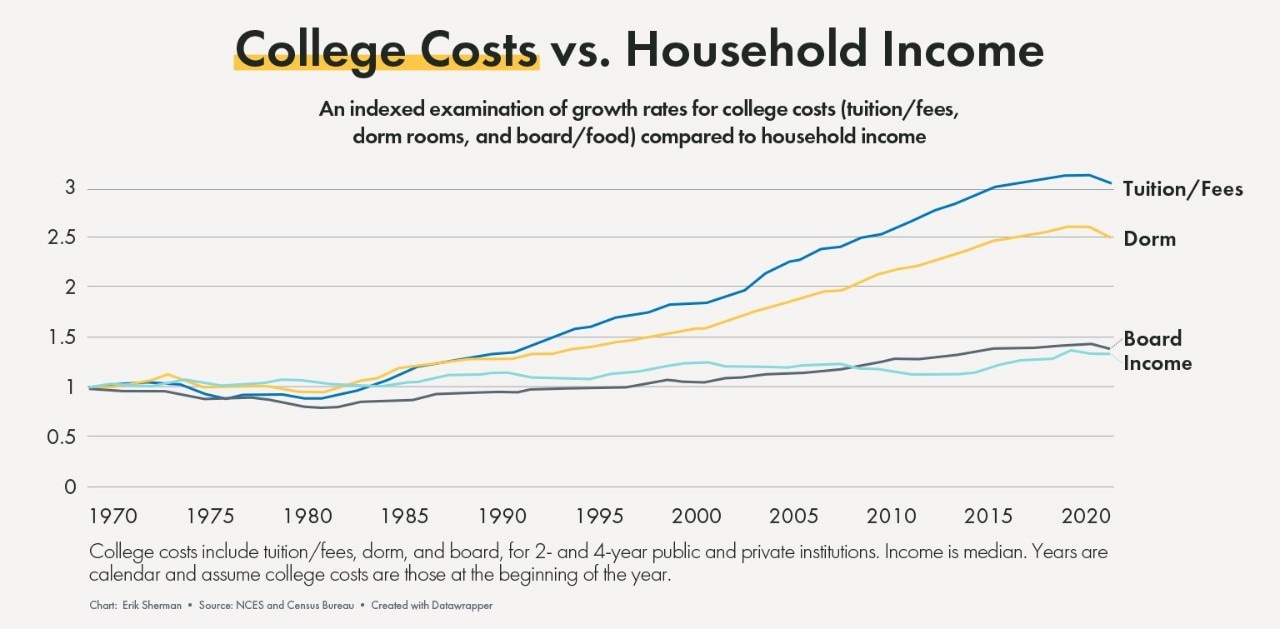

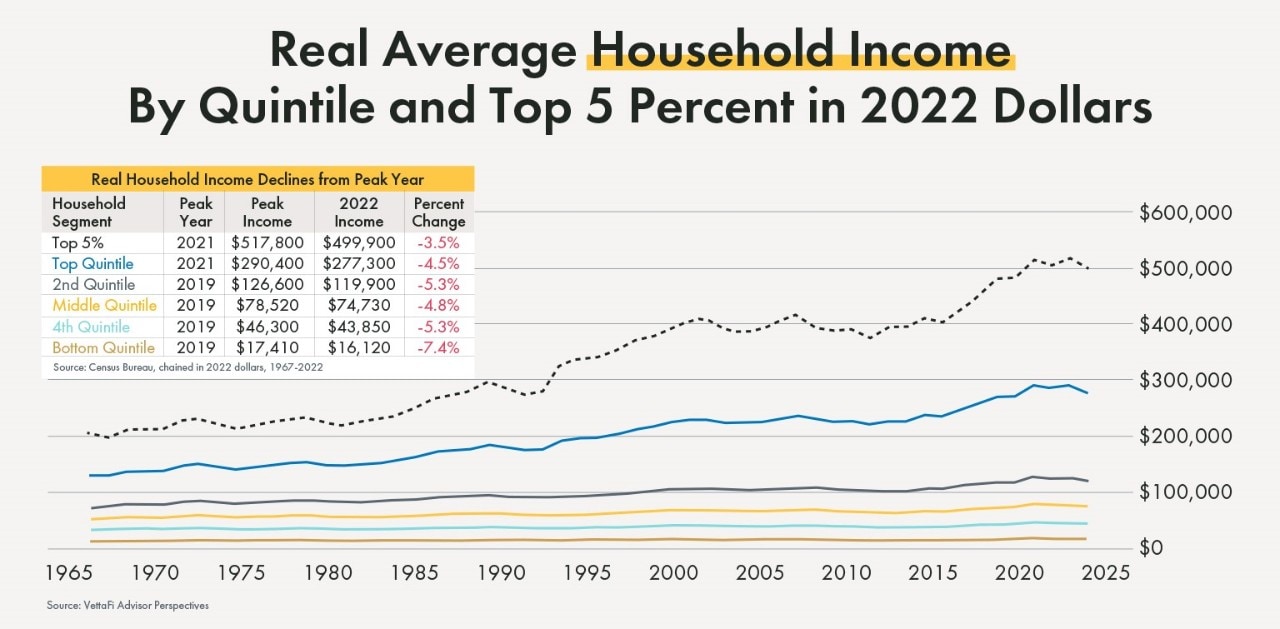

Long before crunching any numbers, clients know what the charts below show: college costs have gone truly exponential in the last one and a half generations, far outstripping increases in the earning power of many high earners and wealthy families.

Faced with the concerning higher education affordability trend, clients often have a strong instinct to do something, anything, to address the problem. As a result, their attention often turns to Section 529 Plans.

In simple terms, then, a 529 Plan is somewhat like a Roth IRA for education. Although there is no income limit on who may make contributions to a 529 Plan, there are total contribution limits that vary state-by-state. (Ohio’s limit is $377,000; the limit for Kentucky and Indiana is $450,000).

Although contributions to 529 Plans are not tax deductible for Federal purposes, they can provide state income tax benefits.1

In addition to income tax advantages in some states, investment earnings inside the 529 Plan are not taxed until withdrawals occur, and distributions made from 529 Plans for qualified educational expenses are not income taxable.

On the downside, distributions from 529 Plans that aren’t for qualified educational expenses are income taxable, and incur an additional 10% penalty.

Clients often have good questions about how best to weigh the tax advantages a 529 Plan might offer (compared to saving for college in a taxable account), against potentially negative aspects of these plans – notably, their restrictions, limits, and fees.2

Let’s suppose that when a child (Harriet) is born to into a family in the highest marginal state + Federal income tax bracket of 44.8%, her grandparents are trying to decide whether to contribute $377,000 to Harriet’s 529 Plan, or instead put it in a trust or other taxable savings “wrapper,” earmarked for college costs.

We built a model to illustrate comparative post-tax, post-fees performance of the two options (the 529 Plan and the taxable account).3

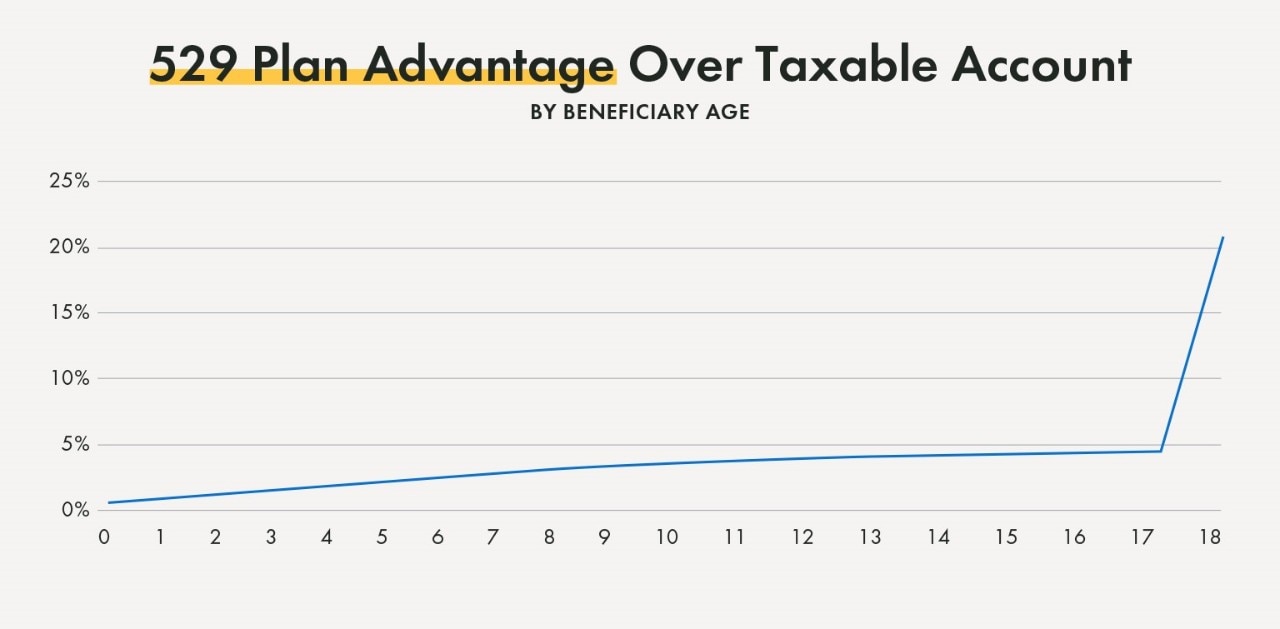

The model suggests that a 529 Plan funded with $377,000 for newborn Harriet might exceed $1.2 million by the time she was 18, while a taxable account would reach approximately $950,000. The net-of-tax advantage for the “fully loaded” 529 Plan versus the taxable alternative is about $250,000 (or 21% of the potential account balance by Harriet’s freshman year).

The chart below shows how most of the 529 Plan’s advantages accrue in a “pop” at freshman year, when withdrawals are taken income tax free.

To understand whether the seeming benefits of a 529 Plan will help you — in short, whether the tax advantages these plans offer are worth it — it’s important to understand what 529 account balances can (and can’t) be used for.

529 account balances can be used to pay qualified education expenses of a designated beneficiary at an eligible educational institution.4

Qualified education expenses include required tuition and fees, and books, supplies, and equipment. Students enrolled at least half-time may also use plan balances for room and board, subject to certain limitations. Up to $10,000 may be used annually for primary or secondary school tuition, and up to a lifetime total of $10,000 may be used to repay principal due on a beneficiary’s student loans.

On the other hand, qualified education expenses don’t include many of the ways families actually launch their children and grandchildren in life, including summer camps, travel team expenses, trips abroad, stipends during unpaid internships, apartment rental around the time of a first job, car expenses, or wedding costs.

Let’s return to the above example of Harriet’s “fully loaded” 529 Plan. Even if she attends a private college for “full freight,” her cost of attendance likely won’t exceed $320,000, and her plan could be overfunded by $850,000. Even if Harriet attended graduate school, it’s unlikely all the funds could be absorbed by qualified education expenses.

Until recently, options for the unused balance would be limited to changing the plan beneficiary to a different qualifying family member, or taking it as taxable income, resulting in a tax on investment earnings that had accrued inside the plan, plus a 10% penalty on those earnings.

Recently enacted provisions in the “SECURE 2.0” Act of 2022 that take effect in 2024 provide a promising opportunity for transferring up to $35,000 in unused 529 Plan balances to a Roth IRA for the 529 Plan’s beneficiary.5

This is a very attractive planning opportunity, because funding a Roth with up to $35,000 before reaching age 30 could put a beneficiary on track for that account to grow to more than $650,000 by age 67. In retirement, the Roth IRA beneficiary could take tax-free distributions and avoid required minimum distributions (RMDs).

Perhaps because this planning option could be so useful, it comes with some limitations.

Because of these restrictions, the 529-to-Roth transfer opportunity is most readily available for “old and cold” 529 Plans funded over a long time period, after the beneficiary has finished college and entered the workforce.

Although the Roth transfer opportunity somewhat reduces risks of overfunding a 529 Plan, in Harriet’s example, her “fully loaded” 529 would still be overfunded by more than $800,000 even after making the $35,000 maximum transfer to a Roth IRA.

Without a doubt, a substantially overfunded 529 Plan is a “high class” problem to have, but it’s still an outcome it’s best to avoid.

Balancing the tradeoff between income tax savings and a potential loss of flexibility is the primary reason Yellow Cardinal encourages families to make 529 Plan funding decisions very thoughtfully, in the context of a comprehensive financial plan.

In that context, 529 Plans can be an important and valuable tool (but not a blanket solution) for education funding, and helping younger generations thrive as they grow up and move into adulthood.

Graphic 1: Adapted from “1982: The Last Time College Costs Kept Pace With Median Income,” by Erik Sherman, Forbes; https://www.forbes.com/sites/eriksherman/2023/07/23/1982-the-last-time-college-costs-kept-pace-with-median-income/

Graphic 2: Adapted from “U.S. Household Incomes: A 50+ Year Perspective,” by Jennifer Nash, VettaFi Advisor Perspectives, Sept. 13, 2023; https://www.advisorperspectives.com/dshort/updates/2023/09/13/u-s-household-incomes-a-50-year-perspective

Graphic 3: Adapted from "Overfunded 529 plans: avoiding too much of a good thing," by Carter Ruml, May 3, 2015; https://kyestates.com/overfunded-529-plans-avoiding-too-much-of-a-good-thing/

1 Ohio allows a state income tax deduction for contributions to the Ohio 529 Plan that can be carried forward, and taken at a maximum of $4,000 per beneficiary per year. Indiana offers a state income tax credit of 20% for contributions up to $7,500 per year to the Indiana 529 Plan, up to a maximum credit of $1,500 per year for joint filers. Kentucky, unfortunately, provides no state income tax deductions or credits for 529 Plan contributions.

2 Investment options in 529 Plans can be relatively limited, and investment options can’t be changed more than twice a year.

3 Model inputs included tax rates, investment costs, projected inflation rates, and 529 Plan costs. The model portfolio was 60% equities, 40% fixed income. Nominal annual returns were projected for equities at 8.6% and for fixed income at 4.3%. The projected annual inflation rate was 2.41%. Annual investment costs were modeled at 0.85%, and additional annual 529 Plan costs were modeled at 0.25%. Stocks were assumed to be held until Harriet reached age 18 and were sold at that time. Bond income was assumed to be taxed each year, and used in part to pay taxes, with the remaining income reinvested in more bonds. To increase simplicity, the model did not include tax effects of periodic rebalancing, and assumed linear investment returns.

4 The designated beneficiary is the student (or future student) for whom the 529 Plan is intended to provide benefits. (From time to time, the account owner can change the designated beneficiary to another family member.) Eligible educational institutions include virtually all accredited postsecondary institutions, as well as schools providing K through 12 elementary or secondary education. For details, see IRS Publication 970, available at https://www.irs.gov/pub/irs-pdf/p970.pdf, pages 50 through 54.

5 See, e.g., Kelly C. Long, “Saving for college: The new 592-to-Roth IRA transfer rule,” Journal of Accountancy (Mar. 6, 2023), and Leonard Sloane, “Parents Have a New Incentive to Fund ‘529’ Plans,” Wall Street Journal (Sept. 2, 2023).

The information on this page is accurate as of November 2023 and is subject to change. First Financial Bank and Yellow Cardinal Advisory Group are not affiliated with any third-parties or third-party websites mentioned above. Any reference to any person, organization, activity, product, and/or service does not constitute or imply an endorsement. By clicking on a third-party link, you acknowledge you are leaving bankatfirst.com. First Financial Bank and Yellow Cardinal Advisory Group are not responsible for the content or security of any linked web page.

The information provided herein is for illustrative purposes and should not be considered investment advice and is not designed to address your investment objectives, financial situation or particular needs. The information is as of the date referenced herein and is subject to change at any time based on market, economic or other conditions. The data represented has been obtained from sources deemed reliable, but we do not guarantee its accuracy or completeness.

You are about to go to a different website or app. The privacy and security policies of this site may be different than ours. We do not control and are not responsible for the content, products or services.

Online banking services for individuals and small/medium-sized businesses.

If you haven't enrolled yet, please enroll in online banking.

Yellow Cardinal resources

* Are not insured by the FDIC. Not a deposit. May lose value.

For businesses already using f1RSTNAVIGATOR online banking.

For clients recently upgraded, who opened a new business account after April 15, 2026, or those joining from BankFinancial or Westfield Bank.