- Not insured by the FDIC or any other government agency

- Not bank guaranteed

- Not a deposit or obligation

- May lose value

There is more to investing than just purchasing a stock and wanting to earn a quick return. Rather, investing should be considered as part of a long-term strategy; one that aligns with your financial goals. Investment planning is one element of a financial plan and begins with a proper understanding of your current financial situation and future goals.

The purpose of investing is to put your money to work with the goal of building wealth over time. To capitalize on investment opportunities, risk tolerance and time horizon are important considerations. The longer your time horizon, the longer your money has to grow. This is often referred to as the power of compounding effect – providing the benefit of time in the market.

Playing the long game has historically yielded higher returns on investment in stocks. But the stock market isn’t the only asset class you might consider. Investors can achieve diversification benefits and target their preferred risk tolerance by varying their portfolios to include real estate, bonds, commodities, and other securities.

Your financial goals shape your investment plan. Applying tried-and-true principles will help you achieve your financial goals.

One basic investment principle revolves around one’s time horizon. As is often said, time in the market is better than timing the market. That’s because history shows that the longer one’s time horizon, two distinct advantages emerge – the probability of loss goes down dramatically and the return predictability goes up significantly.

Financial advisors recommend that investors keep their money in the market for at least five years to weather any storms and achieve acceptable returns.

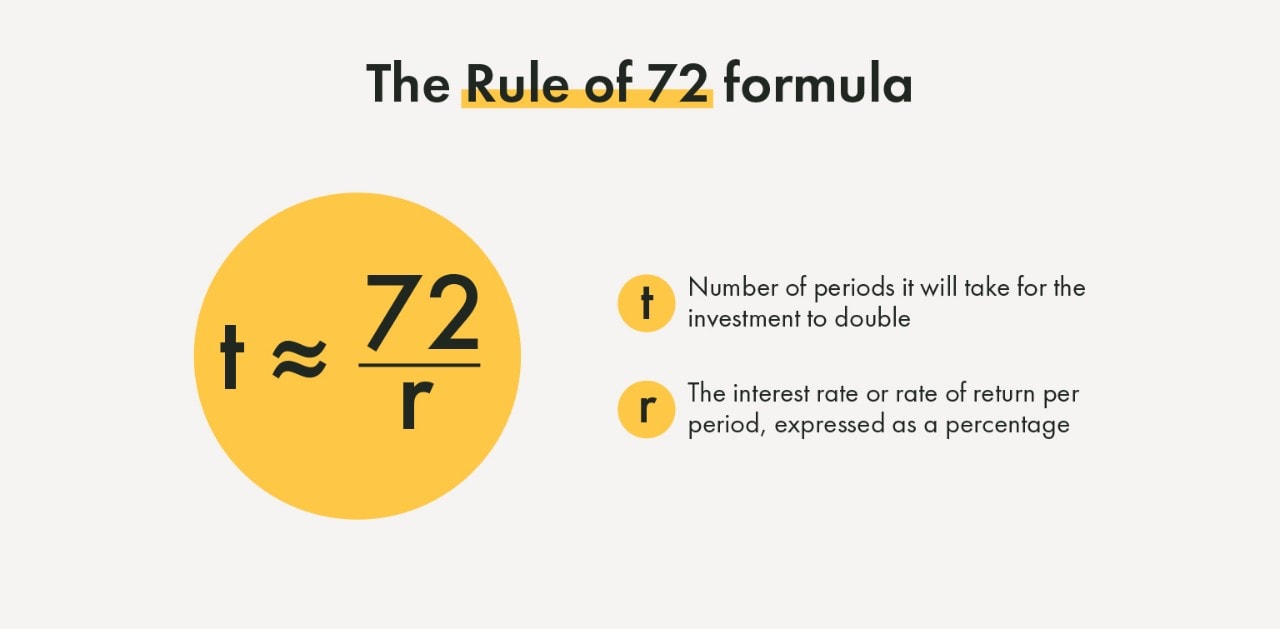

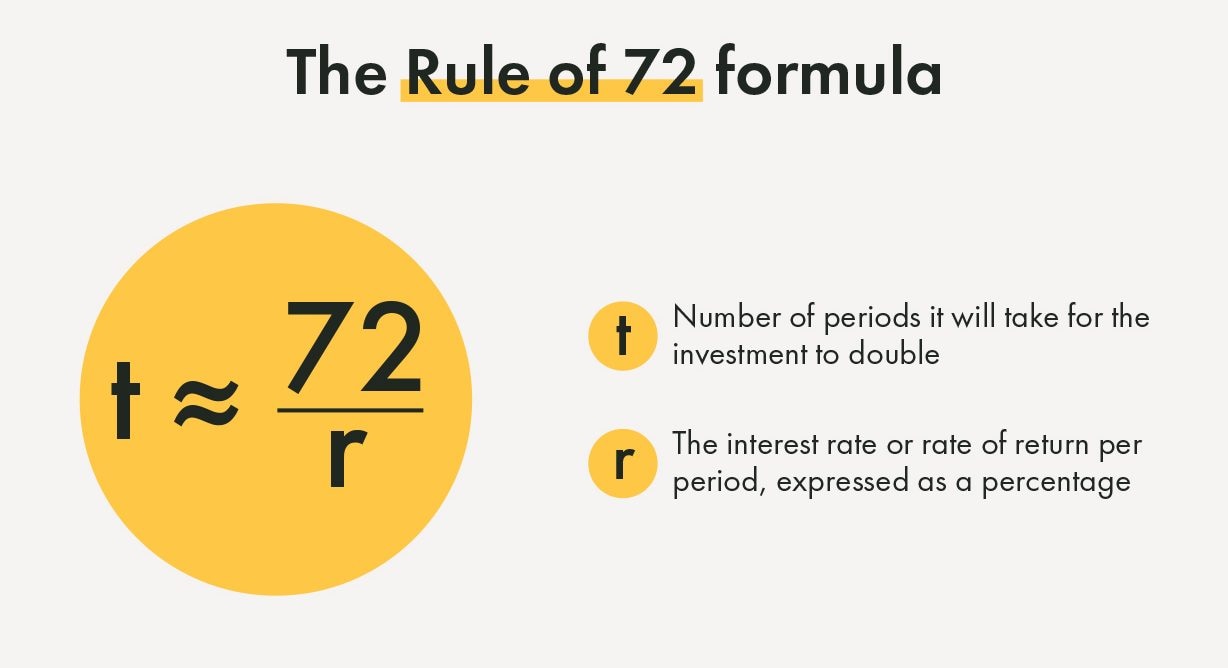

For investments that compound annually, apply the “rule of 72.” Investors use this rule to calculate the time required for an investment to double.

Simply divide 72 by the expected annual rate of return. The result is an estimate of the number of years required for your money to double. For example, imagine a bond’s rate of return is 3%. Dividing 72 by 3 results in 24, the number of years it will generally take for your original bond investment to double.

The rule of 72 is an approximation, but it provides a general expectation of how long it takes to double one’s wealth.

Investors should employ a consistent, disciplined strategy to earn acceptable returns over the long term. Selecting a combination of different asset types can help you achieve your goals while insulating you from market disruptions. With both return and risk as the focus, investment planning should account for your personal goals, financial knowledge, and investment expectations.

Consider your objectives. Are you nearing retirement? Planning to buy a house soon? These decisions inform the types and combination of investments that may be best for you.

If retirement is in the next 10 years, having some exposure to lower risk vehicles such as bonds is common. These securities allow you to protect your nest egg while realizing slow-and-steady gains generated from the coupon payment.

Investing requires controlling one’s emotions. Market volatility can bring out emotional extremes, including fear and greed.

Investment strategies are numerous and can differ widely. While one approach might include a broad emphasis on Diversification another might be more narrowly focused on Momentum or Value style investing. No matter which strategy you implement, controlling your emotions is key. Allow yourself to remain objective so you can make clear long-term investment decisions. Choose an investment method that you’re comfortable with and that you know you’ll stick to through thick and thin.

Working with a trusted partner to implement a cohesive investment strategy is essential. Our wealth advisors at Yellow Cardinal Advisory Group start by taking inventory of your goals, preferences, and risk profile to develop a customized financial plan, which serves as the foundation upon which your investment plan is built.

Working hand in glove with our wealth advisors, our Yellow Cardinal Portfolio Management Team is dedicated to implementing our proven long-term investment approach in client portfolios. This team works tirelessly to combine the right top-down allocation with the right bottom-up securities in order to achieve outcomes that help our clients live their lives on their terms.

Learn more about Yellow Cardinal’s investment philosophy and process.

Rule of 72 graphic: Adapted from “The Rule of 72,” by Elizabeth Aldrich, Business Insider; https://www.businessinsider.com/personal-finance/rule-of-72.

The information on this page is accurate as of July 2022 and is subject to change. First Financial Bank and Yellow Cardinal Advisory Group are not affiliated with any third-parties or third-party websites mentioned above. Any reference to any person, organization, activity, product, and/or service does not constitute or imply an endorsement. By clicking on a third-party link, you acknowledge you are leaving bankatfirst.com. First Financial Bank and Yellow Cardinal Advisory Group are not responsible for the content or security of any linked web page.

You are about to go to a different website or app. The privacy and security policies of this site may be different than ours. We do not control and are not responsible for the content, products or services.

Online banking services for individuals and small/medium-sized businesses.

If you haven't enrolled yet, please enroll in online banking.

Yellow Cardinal resources

* Are not insured by the FDIC. Not a deposit. May lose value.

For businesses already using f1RSTNAVIGATOR online banking.

For clients recently upgraded, who opened a new business account after April 15, 2026, or those joining from BankFinancial or Westfield Bank.