New year, new budget: simple steps to financial bliss

Tips to make your 2026 budget work for you and your lifestyle

With the new year right around the corner, it’s the perfect time to check back in with your budget (or create a new one) and make sure you’re on the right track. It’s all about creating better spending habits and taking control of your money. You’ll have better peace of mind knowing you can have fun and be financially responsible.

Step 1: Determine your income and analyze your spending habits.

Whether you have a single source of income or a couple side hustles that bring in extra cash, add up all the money that you have coming in each month. Then, go through your bank statements and learn your spending habits. Do you have any reoccurring payments? Do you find you spend a lot on random shopping sprees? Look over your payments and try to analyze where your money goes. One easy way is to divide it into 3 categories.

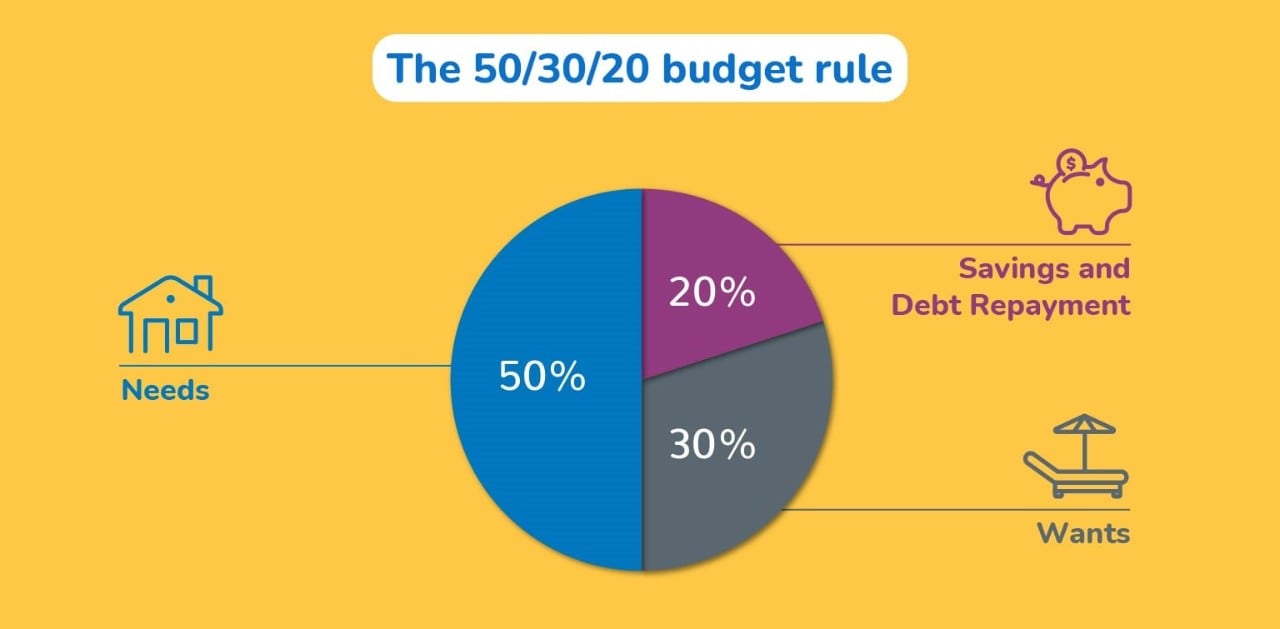

- Needs (bills that must be paid): Mortgage/rent, student loans, credit card bills, car payments, groceries, etc.

- Wants (money spent by choice): Movies, concerts, sporting events, eating out, vacations, subscriptions, etc.

- Savings (money for the future): Money for emergencies, investments, a down payment, and other goals.

Once you understand what category your payments fall under, you can follow what’s known as the 50-30-20 rule: 50% of your budget goes to needs, 30% goes to wants, and 20% goes to savings. This budget serves as good inspiration, but it doesn’t have to be a hard-and-fast rule. The goal is to understand your financial history and understand where your money goes – it’s all about learning what works best for you and your lifestyle.

Step 2: Make a plan to stay on budget with reasonable goals.

So, you look at your bank statements and realize you spend a lot more than you thought eating meals out. You vow to never eat out again. While that might save money, it’s not exactly a realistic goal. Instead, try to see if you can reduce the amount you eat out by half – that way you’re still saving money by cutting back, but not limiting yourself to cooking at home 7 days a week.

This is the time to divvy up your income versus outcome. Do you really need to subscribe to eight different streaming services? Probably not. And there’s a good chance you subscribe to entertainment that you don’t fully take advantage of. If that’s the case, think about cutting out a subscription or two and see how it affects your budget. You might find that you save money without missing out on as much as you thought you would.

It’s also a good idea to comb over all your subscriptions and make sure you know where your money is going (monthly subscription boxes for razors, smoothies, and dog toys...music streaming, magazine subscriptions, gym memberships...you get the gist). You don’t want to look over your bank statements and see that you’ve been paying a monthly fee for a service you no longer use.

Create a budget that works for you. If you believe it’s best for you to eat out in the evenings, try adjusting your spending in entertainment. If you want to continue going on weekend trips, think about saving more while at the grocery. Budgeting is about balancing, and ultimately, saving you the most amount of money in the long run.

Step 3: Make any adjustments and try to build up your savings.

Maybe you want to start investing more into your 401(k) or paying off more than just the minimum payments on your credit card. This is the best time to move your money around and figure out where you want to spend more/less. Minor adjustments may give you the room to save for different goals. You might even be able to start saving for goals like a vacation abroad, down payment, or new car. Not to mention, it’s always a good idea to put money into an emergency fund if you don't already have one. You don’t want to be stranded if your roof starts leaking or your car has an unexpected issue.

Growing your savings may be easier than you think. Here are some easy ideas that might help you save some extra money:

- Shop around for better rates. Reach out to different insurance companies, phone carriers, and internet providers. You may find there are cheaper rates out there that better serve your needs.

- Automate your bills. Some companies provide discounts if you sign up for automated billing – when the money comes directly out of your bank account at the same time each month. At the very least, you don’t have to worry about missing payments that may accumulate interest or affect your credit score.

- Plan your groceries. It may help to make a list of what you need from the grocery store, instead of walking around and seeing what strikes you in the moment. If you know what you need and have meals planned out, you can avoid making unnecessary purchases for food you might not need/want later. There’s nothing more frustrating than spending your hard-earned money on food, then finding it expired in your fridge/pantry. Taking the time to think through your meals beforehand may help you avoid waste down the road.

If you want to start growing your savings but aren’t sure where to start, check out our 12- and 26-week savings challenges. With our 12 weeks savings challenge, you can you can save up to $1,140, and our 26-week savings can help you save up to $1,053. Pick the timeline that works best for you and work to reach your financial goals.

Make 2026 the year to get on top of your finances and change how you think about money. Setting up a budget now will help you develop lifelong skills to work towards financial freedom.

We want to help you flourish. For a personalized approach, get in touch with your local banking center to meet with a financial specialist and build a unique financial strategy.