- Not insured by the FDIC or any other government agency

- Not bank guaranteed

- Not a deposit or obligation

- May lose value

Over 55% of Americans, as a part of a Gallup Poll, reported stock ownership in some form in 2021, reflecting a belief that investing is an important part of financial planning and wealth building. However, portfolio construction designed for your specific wealth goals can be difficult without fundamental knowledge or professional guidance on key investment decisions.

Whether you are a young investor or quickly approaching retirement, take a moment to learn more about different assets, risk preferences, and other tips for building an investment portfolio that will help reach your wealth goals within your comfort level.

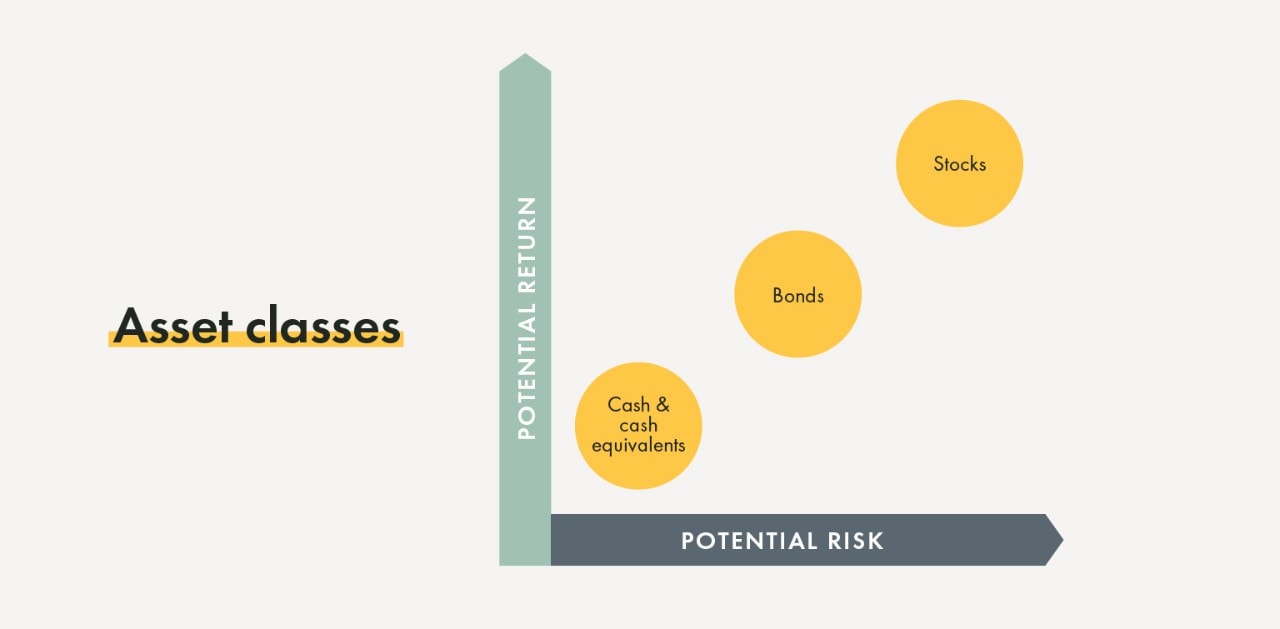

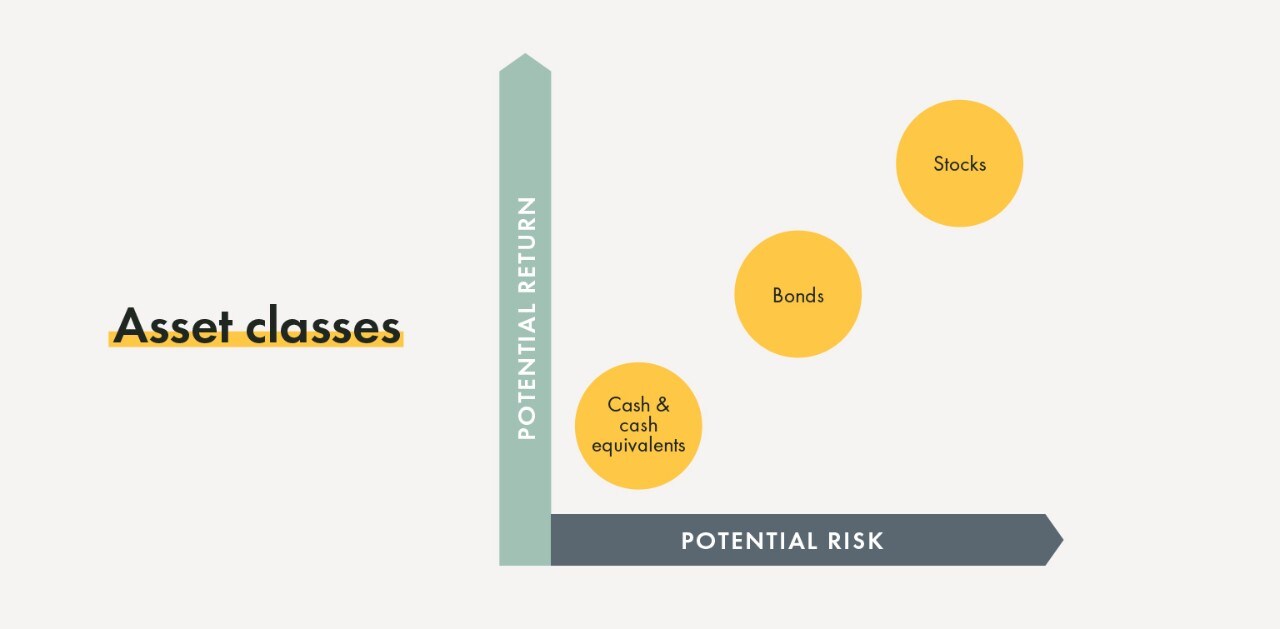

Portfolio construction that meets your wealth goals requires an understanding of the different assets (and their characteristics) that go into creating your investment allocation. Each asset class has its own set of properties that provide certain advantages and risks that you will have to consider along with your wealth goals. Here are some of the most common asset types that you will likely utilize within your investment portfolio.

Stocks, also known as equities, are ownership interests in corporations. In most cases, these are common stock interests in publicly traded companies (i.e., companies that list their stock offerings through an exchange where you can buy, sell, and trade). However, certain accredited investors may also be able to participate in the ownership of closely held stocks, known as private equity.

Equity investments are generally considered a riskier asset class because their value is tied to a wide range of factors that can significantly increase or decrease value over time. However, the potential for growth is what also makes stocks an important part of a portfolio compared to bonds or cash investments.

Bonds, also known as fixed income, is an interest in debt that government institutions and corporations use to raise funds for various projects. Borrowers allow investors to participate in bonds, and in return, investors receive payments of interest based on the amount invested.

Compared to stocks, bonds are typically seen as lower risk and offer a vehicle for storing wealth while also providing consistent returns. Although, bonds can have varying levels of risk depending on the type (e.g., high-yield bonds compared to municipal bonds).

Your portfolio construction can also benefit from a percentage of holdings in cash investments such as:

Despite not providing you with large returns, having cash in your portfolio provides liquidity to meet necessary expenses in the short term and in times of emergency. Furthermore, liquidity can give you the cushion needed to avoid forced sales of your other investment positions during market downturns or inopportune moments. As a result, cash may be considered outside of one’s long-term investment allocation and more of a vehicle for shorter term liquidity needs.

Depending on your net worth and risk appetite, your portfolio may also include a variety of alternative asset classes that represent risk and return profiles that are generally more equity-like in nature – though provide diversification benefits by acting differently than a stock or bond. These investments can often be thought of as insurance against tail risk events such as market volatility and inflation. Alternatives can be further divided between liquid and non-liquid investments – the latter of which can provide the potential for higher returns due to an illiquidity premium but generally come with a much longer time horizon requirement and investor qualifications. Examples of these investments include:

The next step in constructing your portfolio is to identify your risk tolerance and wealth goals, both big and small, that will impact your investment choices and timelines.

Risk tolerance is a measure of the level of risk you are willing and able to accept within your financial portfolio. The main drivers of a person’s risk tolerance tend to include the following factors:

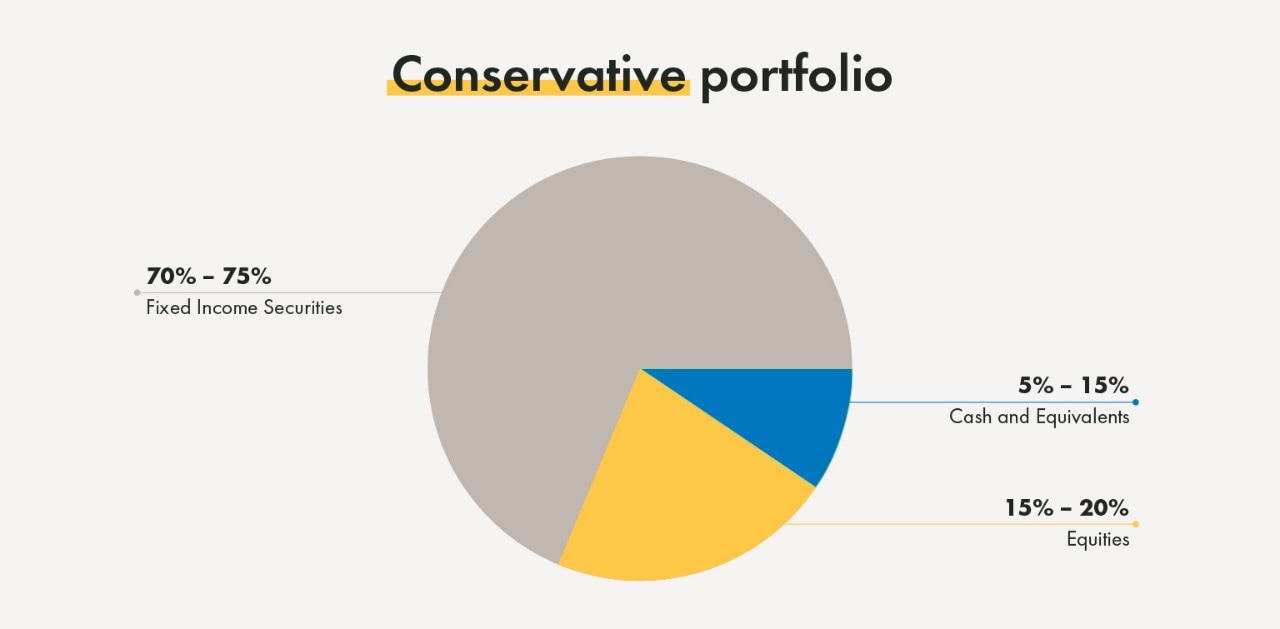

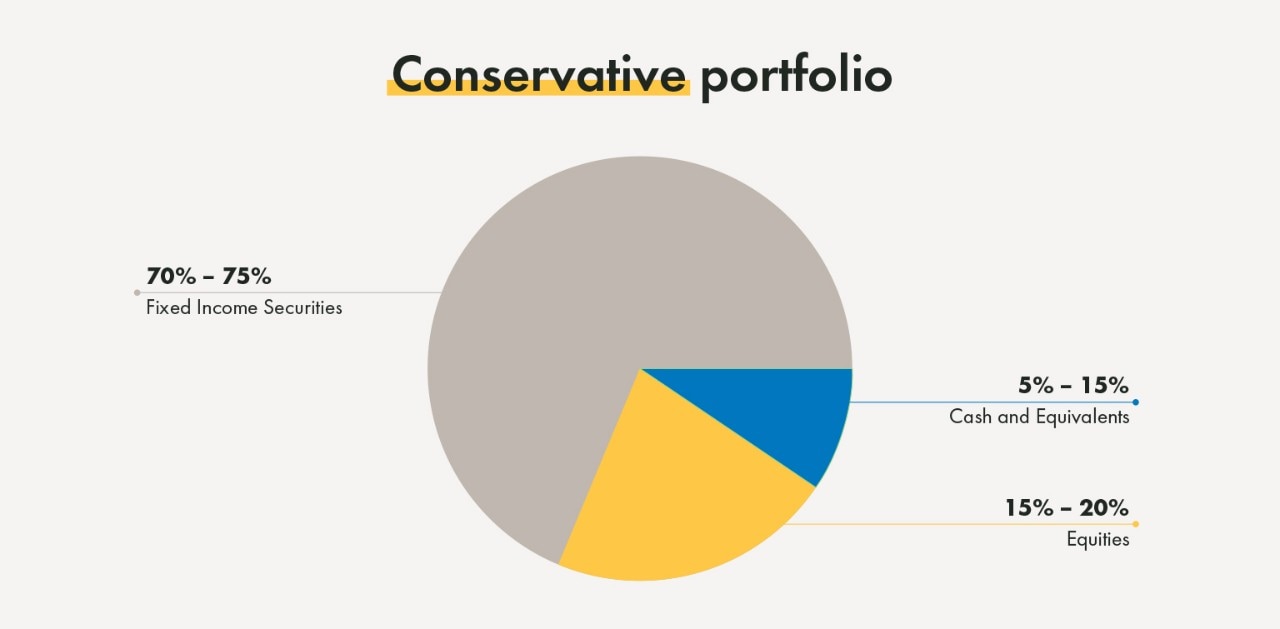

For example, those in or nearing retirement may have a lower risk tolerance because their focus is on preserving their pre-existing wealth to sustain their life in retirement. As a result, they may prefer a portfolio construction with a greater percentage allocated to bonds and cash. In comparison, a younger investor with stable income may have a higher risk tolerance and prefer an allocation with more stocks than bonds.

Along with your risk preference, specific wealth goals and liquidity needs will also guide your portfolio construction. Common wealth goals that may have varying levels of investment allocations could include:

Your wealth goals will help determine the most appropriate investment vehicle for your portfolio (e.g., an IRA vs. a 529 plan) in addition to the specific assets within the portfolio.

In addition to having a portfolio construction with different asset types, having a diverse allocation of investments within an asset class can help you reach wealth goals more safely. In other words, you should own more than one type of stock or one type of bond.

Diversifying is a risk mitigation technique that helps with generating stable growth. For example, you may consider having a combination of small, mid, and large-cap stocks. Other methods for diversifying an asset class include investing in mutual funds, ETFs, or index funds.

Over time, your portfolio allocation will adjust due to changes in your financial situation, risk level, future needs, and market fluctuations. Life changes will also affect your wealth goals over time. In either case, ongoing monitoring and rebalancing your portfolio will be necessary for making sure that your investments still align with your goals.

This is where having a wealth advisor can provide an extra set of eyes to monitor for imbalances in your portfolio, along with offering ideas for rebalancing. Schedule meetings with your advisor one or more times throughout a year to communicate any changes in your finances or other factors that may alter your portfolio. Major life changes may alter one’s long-term investment objective or strategic allocation while near term market risk and opportunities will lead to more tactical adjustments that discretionary money managers will often make.

Portfolio construction is a highly unique process that will vary from investor to investor based on their investment knowledge, risk tolerance, and wealth goals. Our wealth advisors always emphasize holistic and personalized planning that prioritizes investor goals first.

If you have any questions about your current portfolio construction or need help starting your investment portfolio, please consider scheduling an appointment with one of our advisors.

Conservative Portfolio graphic: Adapted from “Four Steps to Building a Profitable Portfolio,” by Chris Gallant, Investopedia; https://www.investopedia.com/financial-advisor/steps-building-profitable-portfolio/

The information on this page is accurate as of April 2022 and is subject to change. First Financial Bank and Yellow Cardinal Advisory Group are not affiliated with any third-parties or third-party websites mentioned above. Any reference to any person, organization, activity, product, and/or service does not constitute or imply an endorsement. By clicking on a third-party link, you acknowledge you are leaving bankatfirst.com. First Financial Bank and Yellow Cardinal Advisory Group are not responsible for the content or security of any linked web page.

The information provided herein is for illustrative purposes and should not be considered investment advice and is not designed to address your investment objectives, financial situation or particular needs. The information is as of the date referenced herein and is subject to change at any time based on market, economic or other conditions. The data represented has been obtained from sources deemed reliable, but we do not guarantee its accuracy or completeness.

You cannot directly invest in an index. Indexes are unmanaged and measure the changes in market conditions based on the average performance of the securities that make up the index. Investing in small and mid-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. Asset allocation and diversification does not ensure a profit or protect against a loss.

You are about to go to a different website or app. The privacy and security policies of this site may be different than ours. We do not control and are not responsible for the content, products or services.

Online banking services for individuals and small/medium-sized businesses.

If you haven't enrolled yet, please enroll in online banking.

Yellow Cardinal resources

* Are not insured by the FDIC. Not a deposit. May lose value.

For businesses already using f1RSTNAVIGATOR online banking.

For clients joining from BankFinancial, Westfield Bank or opening a new business account after April 15, 2026.